Minimum Wage

When Biden or anyone mentions the Dignity of Work the first thing that comes to mind is pay. Its hard to feel dignified if you work full-time and float around the poverty line. However, critics of “artificially” raising the wages by increasing the minimum wage point out that smaller businesses might have a harder time affording labor, larger companies will simply hire less people, prices for goods and services would increase across the board, and a universal nationwide increase neglects regional differences. While the evidence for lower employment and price increases for larger businesses has not shown to be especially prevalent, it does stand to reason that their are regional differences and small businesses might be squeezed with the higher wages. The Fight for $15 might have enough momentum to pass, but I believe being more tactful with the law might provide unexpected benefits and alliances.

The federal government clearly has the power to regulate interstate commerce, so mandating that any company or corporation that does interstate business has to pay their employees at least $15 should be an easy sell. Furthermore, since most business that do interstate business are larger that also protects small business; however, I would go further and make that explicit and say that the minimum wage only applies to interstate companies that make $10 million in revenue or more a year. I would also allow companies that exceed this revenue to still qualify if they take their excess revenue and evenly distribute it to their employees regardless of position. With this distinction the law respects federalism by only targeting companies that do business across state lines and clearly delineates between small and big business. With this delineation further requirements for these large interstate companies will be easier to pass.

Health Insurance

Pay is not the only marker of a job with dignity other benefits like health insurance, vacation days, maternity and paternity leave, and 401ks also help define a good job. With the clear delineation between large and small business, the federal government could also mandate benefits along with wages. Health insurance has the most potential for reform that is beneficial to both employees and employers.

The federal government should reduce the deductibility of health insurance to the average cost of a plan fora household; which I propose should be $6000 for a single adult, $12000 for a married couple, and $15000 for a family with children (details on these costs later). Then the government should mandate that large interstate businesses provide at least $3,000 for full time employees (defined as working 2000 hours or more in a year), and $2000 for part time employees (defined as working between 1000-20000 hours in a year) toward the cost of the medical insurance of their choosing. The company could pay for more to have deduct all the way up to the average cost of a plan from their taxes, but are required to pay the minimum amounts. This is better for employers since instead of having to figure out how to enroll their employees in a medical insurance plan they can just pay the minimum (or more if they wish) and employees get to choose their own health insurance. This helps employers control costs and be able to more accurately predict their expenses. Employees benefit as well since they can choose their own plan and a change in jobs will not be as big of a disruption in their coverage.

Retirement Benefits

The large interstate companies should also be required to provide at least $1500 towards the retirement fund of both part and full time workers. Companies could still match up to employer contributions and the max 401k allowances would still apply, but each year workers would be guaranteed at least $1500 for their retirement accounts, fully vested and irrespective of their own commitments.

Vacation and Unpaid Leave Days

Lastly, vacation and earned leave days should be clarified. It should be mandated that you get an hour of paid vacation for every 20 hours your work and that you earn an hour of unpaid leave (or maybe in the future partially paid leave) for every 4 hours you work. This would be at least 100 hours (2 and a half weeks) of vacation every year if you worked full time and 500 hours (about 3 months) of unpaid leave time. The unpaid leave time could be used as maternity leave, paternity leave, and/or sick days, and you would not lose your job or your benefits while you took the time away. This system is more fair for employers as well as you have to work their to accrue the days. Employees also benefit by having a clear understanding of what benefits they are entitled and how they earn them.

What About the Other Businesses

Advocates for a universal minimum wage might also argue that having these laws only apply to large interstate businesses leaves out a large number of employees who work for smaller or intrastate outfits. This is by design because I believe that small businesses being able to access cheaper labor helps them compete with larger business and helps workers who might have been squeezed out of the labor market due to the higher required compensation. In fact, I would also exempt small business from most other regulation reporting requirements and only investigate them for regulation violations that have actual reported negative impacts. However, to protect workers I would require them to clearly show how their compensation package differed from the minimum compensation package required for large businesses.

So if they paid a lower than minimum wage they would have to report that to their employee before signing and at tax time. Furthermore, if they didn’t offer health insurance or vacation days they would have to tell their employee the value of what they were missing. This would obviously make jobs at companies that offered these benefits more attractive and encourage smaller businesses to compete by offering more creative compensation packages. For example, if a small business wanted to save money by not offering health insurance (saving $3000 in my scenario) they could instead offer $16 an hour which would pay $2000 more for full time work. Or if a small business wanted to offer lower wages like $10 an hour they could offer unlimited leave or more vacation days to compensate. Workers who valued a more flexible schedule or more money might be willing to take these offers.

Why it Works

One might ask if businesses would go along with increasing benefits like vacation days, leave, and retirement funding? They would if they could reduce their health care expenses. Employers cannot control health care costs and because of quirks in our system are still responsible for insuring their employees; in fact about half of the population gets health insurance from their employers. By shifting health insurance from an uncontrollable likely constant increasing cost to a fixed amount employers would save tons of money they could use to raise wages, provide more benefits, and offer more creative compensation packages. Employees would also benefit by not being tied to an employer medical insurance plan they have no input in or control over. These two benefits are frequently used to support the transition to a universal healthcare system. I argue that capping the corporate medical insurance deductibility and mandating a set dollar amount to be used toward employee health insurance accomplish the same thing with far less disruption.

While advocates for $15 an hour might be disappointed that a large portion of businesses are exempt from the minimum wage increase and compensation standards, the vast majority of businesses (around ~65% depending on the revenue of small businesses) would be subject to them and the exempt business would be pressured to increase compensation to compete for labor. Minimum wage detractors who argue that minimum wage increases disproportionately affect certain regional markets, decrease employment, and harm small businesses would find it hard to argue that a law that only affects interstate large business would do the same. In fact, erasing all wage requirements for small businesses should be worth the tradeoff for them and any arguements that multinational corporations like WalMart paying their employees more would reduce employement or raise prices would be a tougher sell.

Nonetheless, their would also need to be more than just laws mandating these requirements their would also need to be government support. By reducing the incentive to provide health insurance their would need to a back stop so that the costs don’t simply shift to the employees eating away at their wage and benefit gains. The next section discusses how small changes to existing government programs would allow these changes and create more opportunities.

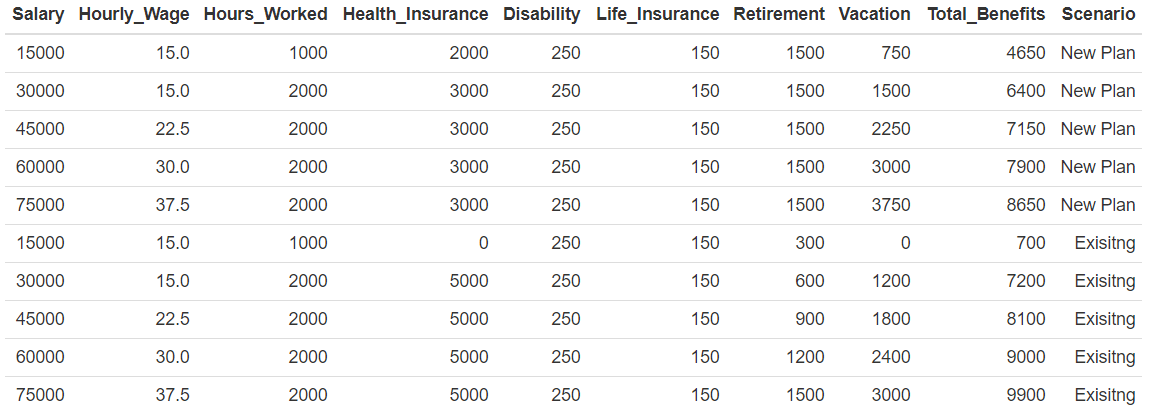

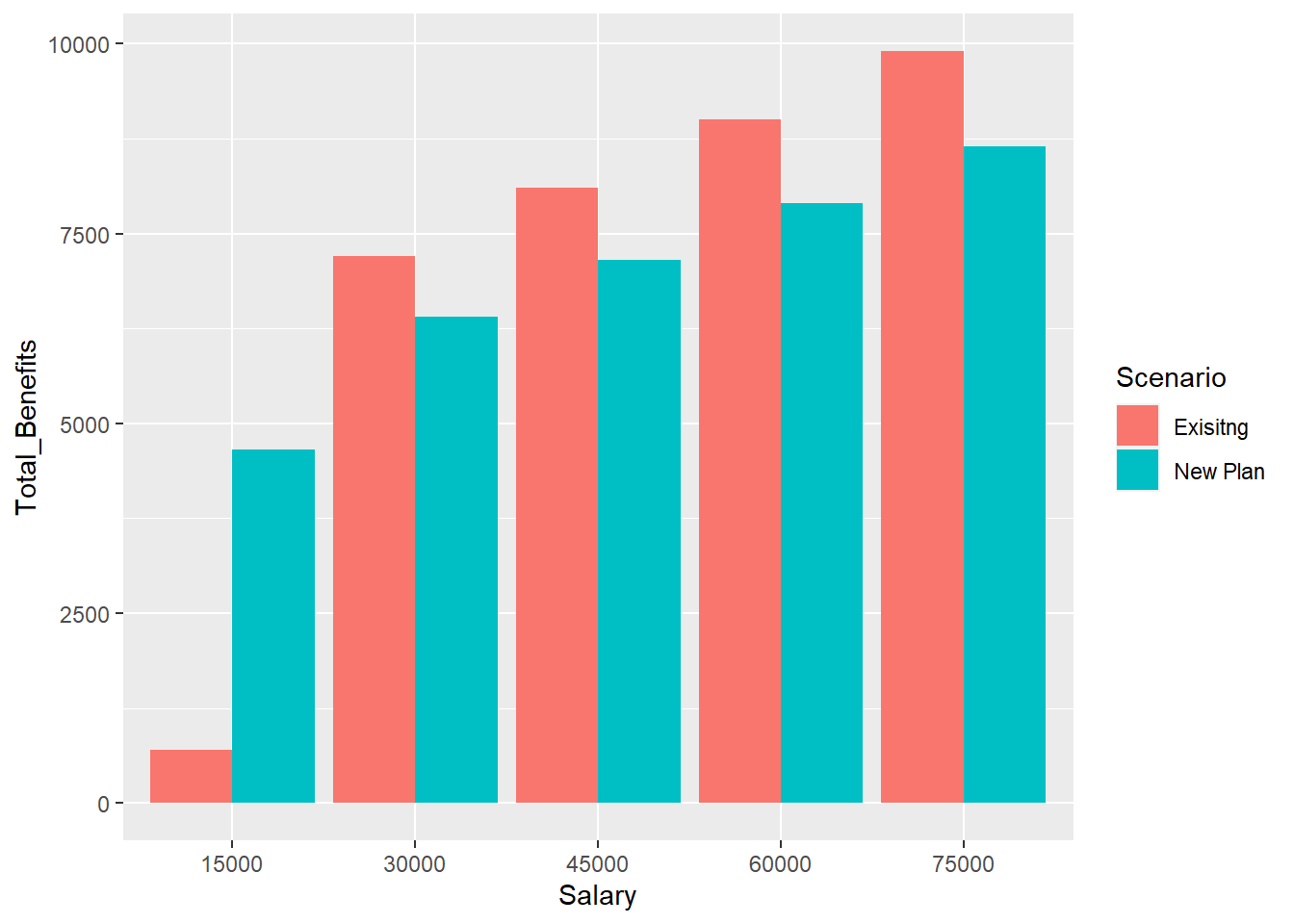

Graphs and Tables

The first graph below compares the cost of the average benefits employees receive to the new proposed benefit plan based on employee wage. The proposed plan reduces total employer compensation for all wages except for the $15,000 employee which represents at least a half time worker who would recieve substantially more benefits than before.

The second graph below compares the cost of the average benefits employees receive to the new proposed benefit plan based on employee wage. Life Insurance and disability remain unchanged. However, the amount paid in vacation pay and retirement increase. Nonetheless, these increases are offset by the dramatic reduction in health insurance premiums. This explains the decrease in overall compensation and shows that employees are getting more benefits but at a lower cost to employers.

The tables supporting these graphs are included as well.

Government Payroll Tax and Health Insurance Reform

Health Insurance

In order for the businesses to be able to pull back from their current medical insurance responsiblities without adverse consequences for employees, the government will have to step in. Luckily their are already systems in place namely Medicaid and the Obamacare subsidies. Biden also wants to create a pubic option, expand Medicare to people 60-64, and reduce prescription drug prices. All of these systems help reduce the cost burden for families; however, they are generally inefficient. By combining the good elements from each of these plans a more efficient and cost-effective plan can be created. That is what Congress has stated they want and have been trying for years; my plan outlines how to get it done.

Medicaid and Obamacare silver plans generally run about $6000 a year per adult and around $3000 a year per child. Since, employees of large interstate business would receive at least $3000 from their employer, either they or a government subsidy would be responsible for the remaining $3000 for single adults. Obamacare has a sliding scale of what percentage of your income should be used for the standard health insurance (the Silver Plan currently, Biden wishes to raise the standard to the Gold Plan) ranging from 2.4% – 9.5% and the government subsidizes the difference.. I would set a rate of a flat 10% of your income toward the standard plan, but half of any employer contribution counts toward your payment and the other half reduces the government subsidy.

So, for example if you were single and made $35,000 in a year and the standard plan cost $6,000, you would be expected to pay 10% of your income or $3500 toward health insurance and the government would subsidize the remaining $2500. However, if you worked for a large interstate business your employer would have to pay at least $3000 towards your medical insurance, half of the employer contribution or $1500 would reduce your payments and the other half would reduce the government subsidy. So in that case you would only be expected to shell out $2,000 while the government would only have to subsidize $1000 of the bill and the employer’s $3000 contribution would handle the rest.

This 10% rate and subsidies based on standard $6000 a year on average plan is more or less Obamacare’s natural evolution. The standard plan would be the public option that anyone could purchase, the subsidy could be used for other insurance plans both cheaper and more expensive but wouldn’t change in size, and the 10% plan is small enough that all incomes could use it which would eliminate the need for another public option for lower income households namely, Medicaid. Since this program would absorb Medicaid, most of the people who get insurance through Obamacare, and a decent portion of businesses who would rather just pay the $3000 (more if they wanted to deduct more from their taxes) then deal with administrative headache of providing medical insurance for their employees. The market power of the public option could be used to standardize prices, lower them, and still provide more services. Simply standardizing the prices so that an MRI doesn’t have widely different prices in two medical centers across the street would be immensely helpful and is one of the arguements for universal health insurance. I argue that this method accomplishes the same while preserving choice for both employers and employees.

I would set the services so they are comparable to some of the best PPO plans with additional benefits to cover basic dental, eye, and mental health. That would mean free yearly visits to your primary care doctor for preventative screenings and birth control (a mandatory part of Obamacare now), a free visit to the dentist for a check up and cleaning, an intake and full visit to a mental health therapist, and a free eye exam and corrective lens. Services would also include free diagnostic tests as necessary including MRIs and CT scans. All generic drugs would be provided for free and any prescription drugs would be a 50/50 split. Most inpatient and outpatient services would be 20% coinsurance after deductible with certain restrictions. Urgent care and other Primary Care visits after the free preventative one would only be a $20-$30 copay and emergency room care would be a $150 copay plus 20% coinsurance after deductible for any additional services. To keep the costs around $6000 for adults and $3000 for kids the deductible and out of pocket maximum would be adjusted yearly, but the services would remain the same.

For single adults this plan more or else keeps the current status quo costs for the government while reducing costs for employers and employees, but what about families? If a married couple both worked full time then it would be more or less the same but if there is one bread winner or a household with kids the calculus changes. I propose setting up a $15,000 standard family plan that includes two adults and any number of children (a married couple with no kids would cost $12,000, the single plan doubled). Each household would be expected to pay 10% of their income towards insurance and the government would subsidize the rest. However, employers would still only be required to pay $3000 per worker, if both adults work that would be $6000 towards the costs, but if only one adult worked it would still only be $3000 leaving a bigger bill for the government to pick up. Nonetheless, while the employer is only required to pay $3000 per worker they still get deductions for up to the full $15,000 family plan, so a worker could negotiate for the full amount and higher paid workers would expect it.

Regardless, even if we assume that 100 million of the 122.8 million households in the United States received an average subsidy of $3000 that would only cost $300 billion about 25% less the current Medicaid costs. Furthermore, by reducing the amount an employer can deduct for health insurance and giving them the option to pay only $3000 the amount of the employer sponsored health insurance tax expenditure would dramatically decrease, possibly by as much as half.

Entitlements

While health insurance gets a lot of press because of the costs and inefficiencies, the entitlement programs have some of the same problems. Medicare spends almost $12,000 per person and a big portion of those costs are prescription drugs. Furthermore, up to 25% of Medicare expenses are for the last year of beneficiaries. NIH. Medicare, with its huge market power, is currently the basis for most of the medical prices in the Us. However, because most of their patients are older they deal with a different set of problems. If Medicare was used to supplement the public option instead of replace it once people reached old age it could save a lot of money.

I propose that Medicare transforms from a full insurance to an insurance expansion on top of the public option proposed above. The new Medicare would cover all prescription drugs, but negociate the prices of them to reduce costs. Furthermore, it would fully cover hospice care and lower the deductible and yearly out of pocket maximum so that older beneficiaries who use more medical services aren’t constantly paying high out of pocket costs. They would still be expected to spend 10% of their income for health insurance up to the cost of the standard plan (including any income they got from Social Security), but they would also receive the Medicare expansion on top of that. I would try to keep the Medicare expansion valued at $3,000 per beneficiary and adjust the cost based on the deducible and out of pocket maximum which would give older Americans an insurance valued at around $9000 a year. Since Medicare costs would only be $3,000 for each of the around 60 million people Medicare covers currently would only cost about $180 billion a far cry from the almost $651 billion it costs now.

The other big entitlement, Social Security, provided an average benefit of $1505 a month to retirees and served 64 million people last year and as a result cost over $1 trillion. Social Security was originally designed as a anti elderly poverty program and has somehow morphed into a partial income replacement program where the benefits you can expect to receive are based on how much your earned working.

I propose reverting back to an anti poverty measure where if you worked 40 years before first withdraw and paid into the program at some minimum income you get the full benefits, if you work 10 years you get half the benefits and if you work 55 years you get 125% of the full benefits. All the other years would be prorated accordingly so that benefits increase by 25% of the full benefit every 15 years of working past the initial 10 years and the full benefit would be set at around the elderly poverty line which is around $12,000. Around 45 million retirees, 3.6 million widowers, and 8.4 million disabled workers benefit from social security. They and a few other groups bring the grand total to 64 million beneficiaries. If every one of the beneficiaries received the full $12,000 a year benefit it would cost $832 million much less than $1 trillion and partial benefits based on various qualifiers would reduce that amount further.

Since this is clearly a reduction in benefits for the more well off it would meet significant resistance for those near retirement who would see their benefits drop. To negate this there should be a phase in period where people can choose between the programs as long as they start collecting benefits at age 67. If they collect benefits sooner or choose to opt into the program than they will be automatically enrolled in the new program even if they qualified for the old one. This option should temper the harshest critics.

The savings in the entitlement costs would lower entitlement expenditures from the $1.7 trillion spent now to the a little over $1 trillion dollar savings almost $700 billion a year. These savings could translate to payroll tax cuts reducing costs for employers and employees leading to more take home money and higher pay. The payroll tax rate currently set at 15.3% split evenly between employee and employers (12.4% for Social Security, 2.9% for Medicare) could be reduced to a flat 10% (8% for Social Security and 2% for Medicare). The existing system currently exempts income above a certain threshold for Social Security tax and adds a surcharge for income above a certain threshold and investment income for the Medicare tax. I would eliminate both of those thresholds and tax all income at the strict flat rate of 10%. This leaves plenty of wiggle room for unexpected cost increases and represents a dramatic reduction in payroll taxes paid by both businesses and employees. Furthermore, the entitlement cost reduction would also result in less deficit spending to make up for the gaps that the payroll taxes wouldn’t cover.

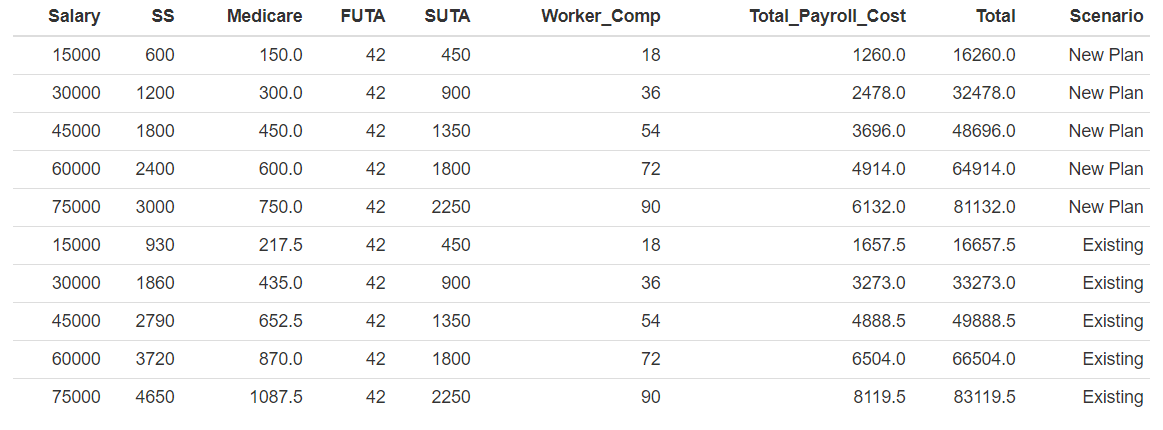

Graphs and Tables

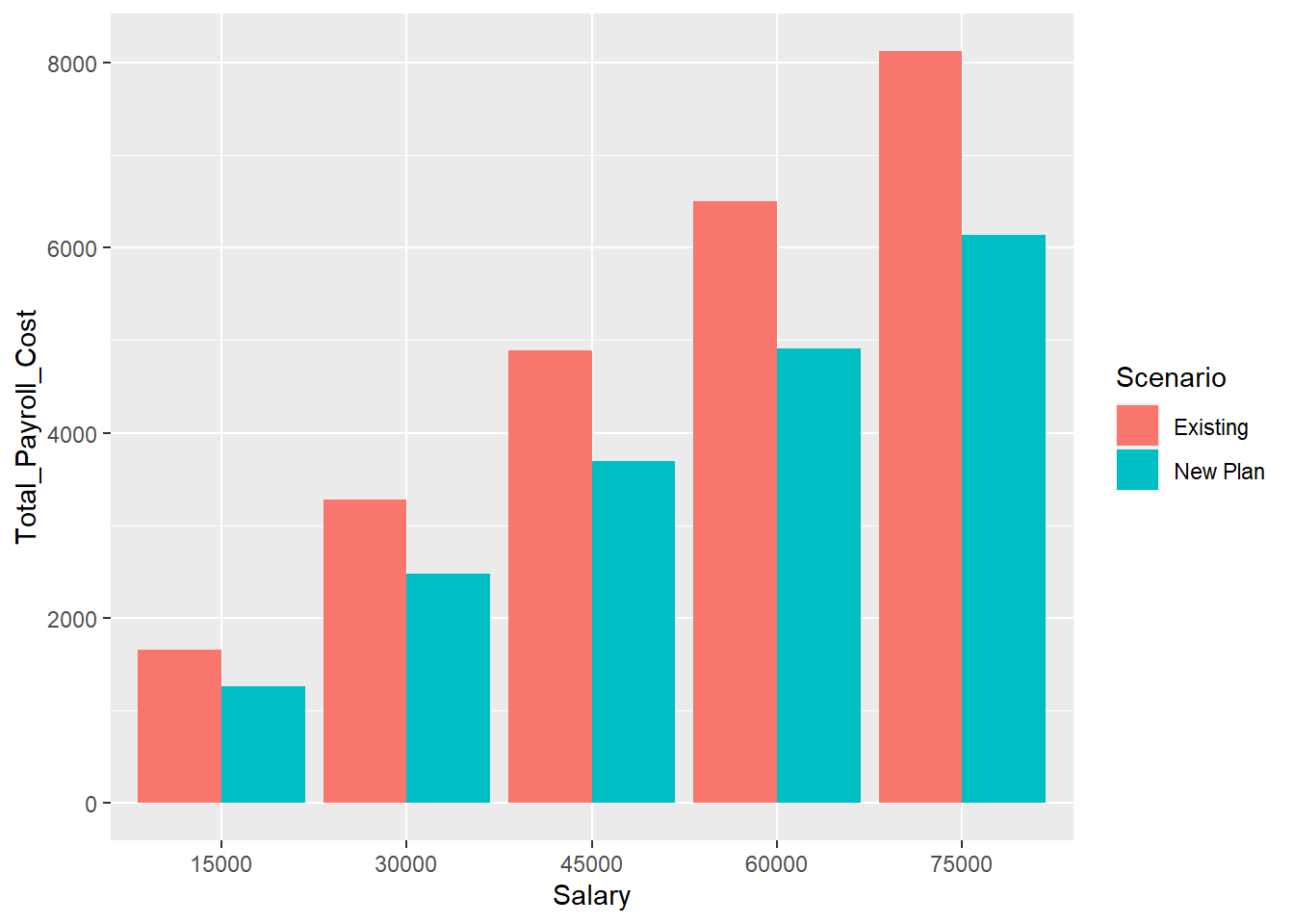

The first graph below compares the current payroll taxes employers pay to the new proposed plan based on employee wage. The new plan substantially reduces the amount employers pay in payroll taxes.

The second graph below compares the current payroll taxes employers pay to the new proposed plan based on employee wage. Insurance programs that cover unemployment and disability like FUTA, SUTA, and Workers Comp remain unchanged. However, there are huge differences in the amount paid to Social Security and Medicare reducing employers costs dramatically.

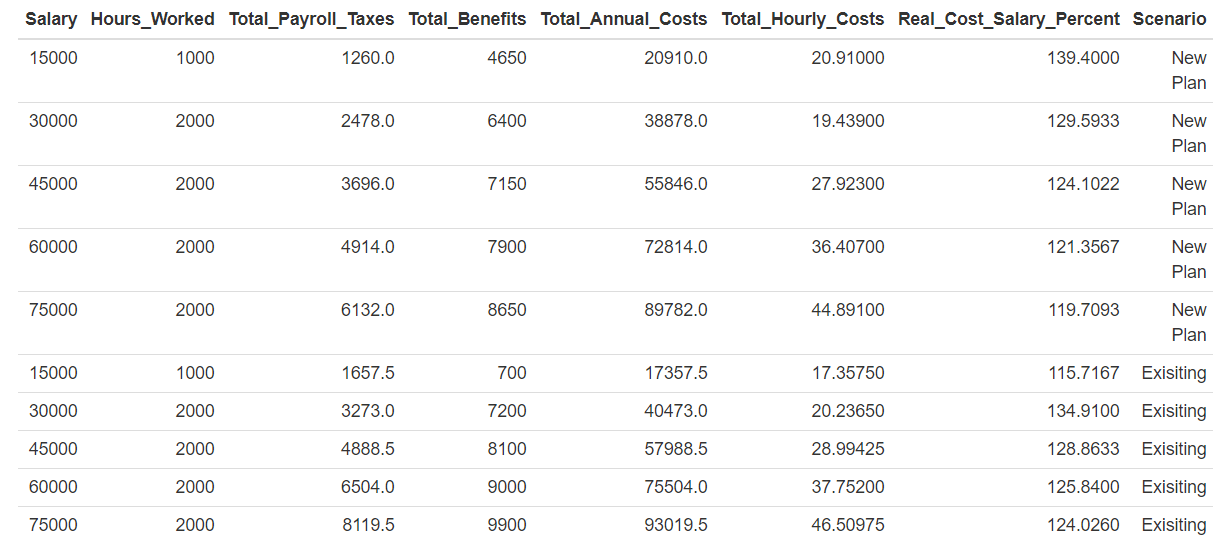

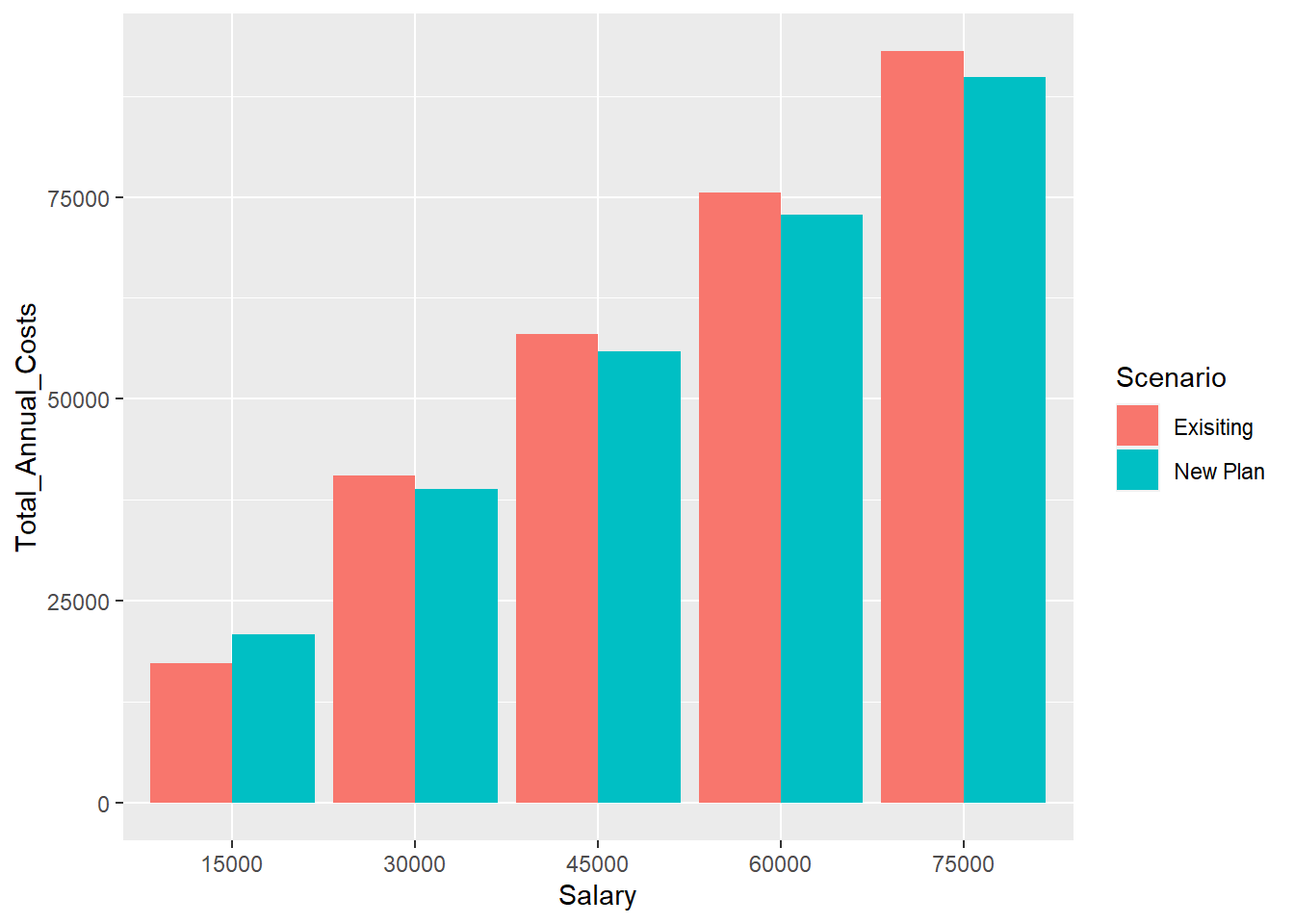

The third graphs compares the total employer costs including payroll taxes and benefits of the existing scenario to the proposed plan. The new plan saves the employer money in all wage cases except for the $15,000 case which represents a half time worker who is receiveing benefits they wouldn’t be otherwise.

The fourth graph breaks down the total employee compensation by salary, total benefits, and payroll tax payments by the employer. These show that reductions in compensation aren’t coming from a dip in take home pay but mostly from benefit reduction in the form of health insurance and a decrease in payroll taxes.

The tables that inform these graphs are also included.